When you’re in the market to buy a home, the type of mortgage you choose can significantly shape your financial future. While many first-time buyers simply default to a 30-year fixed-rate mortgage, there’s another option that deserves a close look—especially in certain market conditions: the adjustable-rate mortgage (ARM). Both have their merits. Both come with trade-offs. And at CapCenter, we believe you deserve a clear, side-by-side look at how they actually compare—without the jargon, fine print, or hidden costs.

Let’s break it down.

Understanding the Basics

Fixed-Rate Mortgage

A fixed-rate mortgage is exactly what it sounds like. The interest rate you agree to at the start of the loan remains the same throughout the life of the loan. Whether you’re taking out a 15-year or 30-year mortgage, the rate won’t change, which means your monthly principal and interest payment stays consistent.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage, on the other hand, starts with a fixed interest rate for a set number of years (often 5, 7, or 10). After that initial period, the rate adjusts—usually once a year—based on market conditions. That means your payment could go up… or down.

The Appeal of Each Option

Why Buyers Choose Fixed-Rate Mortgages

1. Predictability

With a fixed-rate loan, your monthly housing payment is stable and easy to budget for. Even if interest rates spike years down the line, your mortgage payment won’t change.

2. Long-Term Peace of Mind

If you plan to stay in the home for 10+ years, a fixed-rate mortgage removes uncertainty and ensures you’re not at the mercy of rate changes down the line.

3. Simplicity

There are no adjustment caps, indexes, or margin rates to monitor. A fixed-rate mortgage is straightforward, which is one reason it's the most common choice.

Why Some Buyers Opt for ARMs

1. Lower Initial Rates

ARMs typically offer a lower starting interest rate than fixed-rate loans. This can mean significantly lower payments during the initial fixed period, helping you save or qualify for a more expensive home.

2. Short-Term Advantage

If you’re not planning to stay in the home long-term—say, you’re buying a starter home or expect to move within 5 to 7 years—you may never experience a rate adjustment. That means you benefit from the lower rate without the risk of a future increase.

3. Strategic Flexibility

In declining or stable rate environments, some borrowers leverage ARMs to refinance into a fixed-rate loan before their rate adjusts upward. Others use the monthly savings during the early years to pay down other debt or invest elsewhere.

What Drives the ARM Adjustment?

After the initial fixed period, your interest rate adjusts based on a pre-determined index (like the Secured Overnight Financing Rate, or SOFR) plus a margin (a fixed percentage set by your lender). ARM loans also come with limits—called caps—on how much your rate can increase at each adjustment and over the life of the loan. For example, a 5/1 ARM with 2/2/5 caps might adjust like this:

- 5: Fixed for the first 5 years

- 1: Adjusts annually thereafter

- 2: Max rate increase at first adjustment

- 2: Max rate increase at each subsequent adjustment

- 5: Max total increase over the life of the loan

Understanding these limits is essential, especially if you're approaching the end of the fixed period in a rising rate environment.

Which Mortgage Is Right for You?

There’s no one-size-fits-all answer. But here are a few guiding questions to help you decide:

How long do you plan to stay in the home?

If you’re buying a “forever home,” the predictability of a fixed-rate mortgage is often worth it. But if you’re buying with a shorter horizon—relocation, career change, or growing family in mind—an ARM could provide savings you’ll actually realize.

Are you comfortable with risk?

Some people sleep better knowing their payment will never change. Others are comfortable with uncertainty, especially if it brings short-term financial advantages. Neither approach is wrong—but one might fit your personality better.

What direction are interest rates headed?

If rates are high today but expected to drop, an ARM might give you flexibility to refinance into a lower fixed rate later. If rates are low now and you want to lock them in, a fixed-rate mortgage could be your safer bet.

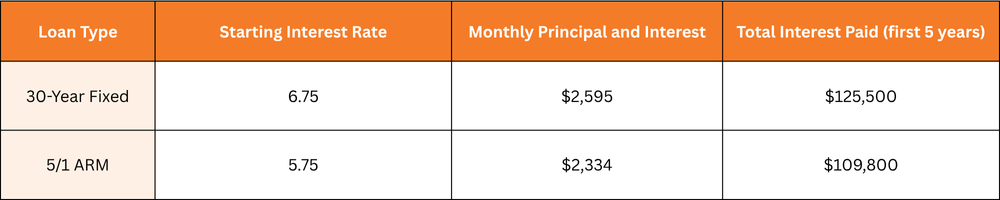

A Closer Look: Real-World Payment Comparison

Let’s take a hypothetical scenario and compare monthly payments for both loan types. We’ll assume a $400,000 loan amount with a 20% down payment and a 30-year term.

Over the first five years, the ARM borrower pays over $15,000 less in interest—and saves more than $250/month. But once the fixed period ends, their payment could increase depending on market rates.

Hidden Cost Consideration: Closing Costs

Here’s something most borrowers overlook: switching from a fixed to an adjustable—or vice versa—later typically involves refinancing. And that means paying closing costs again.

Unless you’re working with CapCenter.

We pioneered the Zero Closing Cost Mortgage nearly three decades ago, and we’ve helped tens of thousands of homebuyers save thousands upfront by eliminating origination fees, application fees, appraisal fees, title settlement fees, and more. So whether you’re choosing a fixed-rate or adjustable-rate loan, CapCenter clients never have to worry about paying again just to make a smarter choice down the line.

That means you could take advantage of today’s lower ARM rates and refinance into a fixed-rate mortgage later—without a cost penalty.

When ARMs Went Wrong (and Why That’s Less Likely Today)

During the 2008 financial crisis, adjustable-rate mortgages got a bad reputation—and for good reason. Many of the ARMs offered in that era came with no caps, little to no income verification, and sky-high margins. When rates reset, monthly payments doubled or tripled. That’s not what we’re talking about here.

Today’s ARMs are far more regulated and transparent. Caps are built-in. Borrowers must qualify fully, not just for the teaser rate. And lenders like CapCenter will walk you through your maximum possible payment so you’re never caught off guard.

Final Thoughts: Fixed vs. Adjustable

If you prioritize predictability and plan to stay put for the long haul, a fixed-rate mortgage may be the best fit. But if you want to maximize your savings in the early years—or expect to refinance or move before your rate adjusts—an ARM can offer a powerful financial advantage.

The key is understanding your personal timeline, your risk comfort, and your long-term goals. No two buyers are the same. At CapCenter, we help you weigh your options without pressure, always keeping your best interest (and your wallet) in mind.

Why Buyers Choose CapCenter—Fixed or Adjustable

At CapCenter, we’re more than a mortgage lender—we’re a long-term financial partner. Whether you’re drawn to the stability of a fixed-rate loan or intrigued by the short-term savings of an ARM, we help you make the right call for your life, not just your loan.

With Zero Closing Costs, in-house processing, and a reputation for expert guidance, you’ll get a mortgage experience that’s transparent, affordable, and fast.

🧠 Ready to compare loan options?

Try our free tools:

Or talk with a mortgage consultant today. No pressure. No nonsense. Just smart advice.

FAQs

Is an ARM riskier than a fixed-rate mortgage?

It can be, but it depends on how long you plan to stay in the home and how comfortable you are with possible payment changes. Today’s ARMs have built-in protections, and CapCenter helps you understand every scenario before you commit.

Can I refinance from an ARM to a fixed-rate later?

Absolutely. And with CapCenter, you can do it with zero closing costs, making refinancing a smart move—not an expensive one.

What’s the most popular mortgage type?

Fixed-rate loans remain the most popular, but ARMs can be a better fit in certain market conditions. It’s worth discussing both with your mortgage consultant.